Financial fraud is rising at an unprecedented rate worldwide. The explosion of digital payments, e-commerce, online banking, and e-wallets, combined with advancements in technologies such as AI and deepfake, has made financial fraud more complex and difficult to detect.

According to the Federal Trade Commission (FTC), consumer-reported losses due to fraud increased by 25% in 2024 compared to the previous year, reaching $12.5 billion. Simultaneously, Coinlaw.io predicts that global losses from online payment fraud will exceed $50 billion in 2025, with approximately 3.3% of global digital payment transactions involving fraudulent activity.

1. What is Financial Fraud?

Financial fraud refers to the act of deceiving victims in order to unlawfully seize their assets or sensitive information. This often involves tricking the victim into acting quickly, such as entering an OTP, scanning biometric data, or transferring funds fraudulently. Along with financial theft, personal information, such as bank account numbers, identification numbers, or passwords, is also targeted to facilitate asset theft.

The growth of artificial intelligence (AI), e-commerce, digital payments, and other technologies has opened the door to more sophisticated and damaging financial fraud schemes.

2. Common Types of Financial Fraud

While there is no exact report on the total number of types of financial fraud, they can generally be classified into several prevalent forms:

2.1. Identity Theft

Identity theft occurs when fraudsters illegally acquire and use another person’s sensitive information, such as ID numbers, bank account details, credit card information, email addresses, or biometric data, for fraudulent purposes. Common identity theft methods include:

- Phishing: Fraudsters send emails, text messages, or social media messages that appear to be from legitimate sources to trick victims into revealing sensitive information.

- Data Breaches: Hackers infiltrate company databases and steal personal information, which is either sold on the black market or used for fraudulent activities.

- Skimming: Fraudsters attach devices to ATMs or point-of-sale terminals to collect card details during legitimate transactions.

- Mail Theft: Criminals steal physical mail, such as bank statements or credit card offers, to gather personal information.

- Social Engineering: Fraudsters impersonate bank employees, government officials, or trusted organizations to trick victims into providing private information. According to GASA 2024, 75% of victims lose money through social engineering.

2.2. Payment Fraud

Payment fraud is one of the most widespread forms of financial crime, affecting both individuals and businesses around the globe every day. Criminals manipulate payment systems to steal money, defraud sellers, or exploit banking system vulnerabilities, often causing severe consequences. In the third quarter of 2024, U.S. consumers reported losses of $58 million, according to industry estimates.

Common methods include:

- Card-Not-Present (CNP) Fraud: Fraudulent transactions made online using card information. According to Nilson Report, CNP fraud accounts for over 70% of global card fraud.

- Credit Transfer Fraud: Fraudsters impersonate bank employees, government officials, or business partners to transfer funds unlawfully.

- Real-Time Payment Fraud: Fraud related to instant payment transactions. Europol has warned that this is a growing fraud trend in Europe.

- Payment Diversion Fraud: Fraudsters divert money from legitimate transactions into their own accounts.

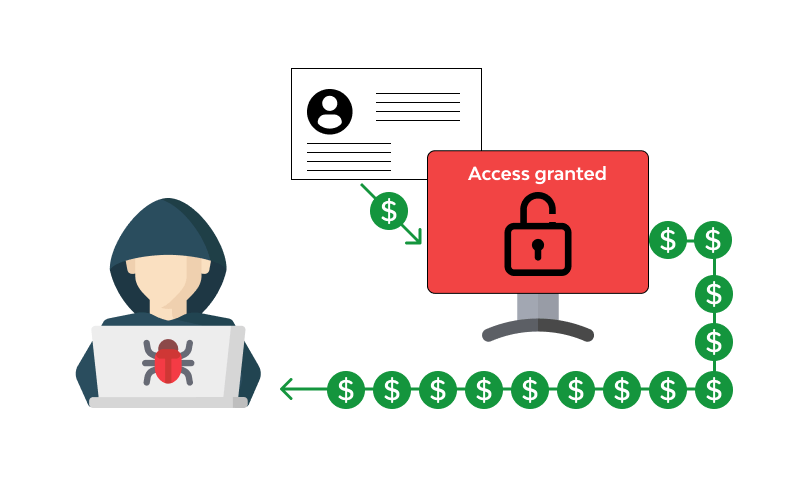

2.3. Account Takeover (ATO)

ATO occurs when fraudsters gain control over a victim’s online account, such as a bank account, email, or social media account. Criminals typically gain access through brute force attacks, credential stuffing, phishing, malware, or by purchasing stolen data. Once they have access, they can withdraw or transfer money without authorization, change account details (such as phone numbers or email addresses) to maintain long-term control, or impersonate the victim to defraud others. According to reports from Experian & TransUnion, the APAC region has seen a 70% increase in ATO cases between 2023 and 2024.

Common signs of ATO include:

- Unusual login activity

- Multiple failed login attempts

- Unauthorized changes to account details

- Unrecognized transactions

- Logins from new devices or locations

- Emails notifying changes to account security that the user did not initiate

2.4. Investment Fraud

Investment fraud schemes often involve sophisticated tactics designed to deceive individuals into believing they are making legitimate, low-risk investments offering high returns. In 2024, the FTC reported that consumers lost over $5.7 billion to investment fraud, a $1 billion increase compared to the previous year.

Fraudsters use various techniques, including AI-generated content for convincing advertisements and deepfake technology to impersonate celebrities in fraudulent campaigns. Regulatory bodies predict that AI will be increasingly exploited for fraud in 2025 and 2026.

2.5. Mobile App Fraud

The widespread use of digital banking has facilitated the rise of fraud involving mobile apps. Common methods include:

- Fake Banking Apps: Fraudulent apps that mimic legitimate banking apps to deceive users into providing their personal information.

- Overlay Attacks: Fraudsters place fake interfaces over legitimate apps to collect sensitive data.

- SIM Swap: Fraudsters swap SIM cards to take control of a victim’s bank account. According to Kaspersky, SIM swap fraud increased by over 60% in many Southeast Asian countries in 2024.

Financial fraud is becoming an increasingly serious global issue. The development of advanced technologies has made it easier for fraudsters to carry out sophisticated and complex schemes, resulting in enormous financial losses. Both organizations and individuals must adopt advanced security solutions and raise awareness to prevent these attacks.

Savyint offers a comprehensive Fraud Management System (FMS) platform that integrates real-time fraud detection, enhancing the security of transactions. This system helps businesses build strong customer trust by minimizing fraud risks, protecting sensitive customer data, and strengthening security in all transactions.

Connect with Savyint experts today to mitigate all financial fraud risks!

Sources:

- Federal Trade Commission (FTC). (2024). Consumer Sentinel Network Data Book

- Coinlaw.io. (2024). Global Payment Fraud Report 2025

- Europol. (2024). European Cybercrime Centre Report

- Kaspersky. (2024). Mobile Security and Fraud in Southeast Asia

- 8 Types of Financial Fraud to Look Out for in 2025, Sumsub