Small and medium-sized enterprises (SMEs) are vital to the economic development of any nation, playing a key role in creation and contributing significantly to national budget revenues. However, access to finance remains a persistent challenge for SMEs in many countries. The advent of open banking is expected to break down many financial barriers that SMEs face.

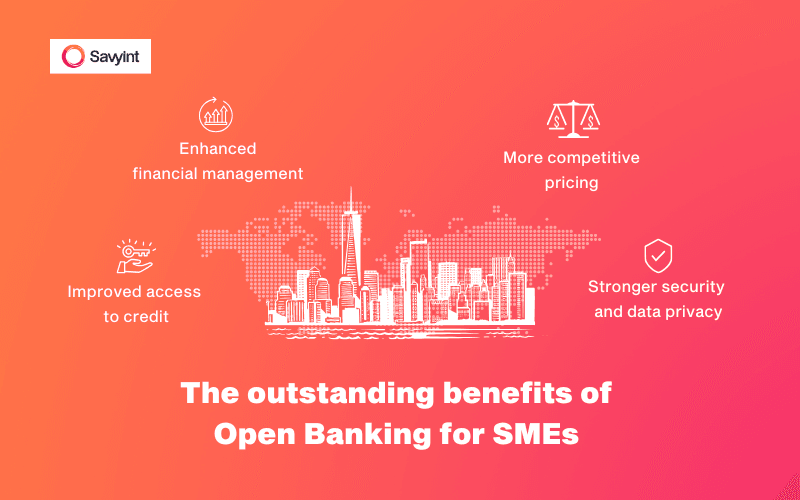

The outstanding benefits of Open Banking for SMEs

Open banking not only benefits banks, third-party providers and end-users, but it also delivers significant advantages to SMEs.

Improved access to credit

SMEs often struggle to obtain credit from traditional banks due to factors such as lack of audited financial reports, insufficient collateral or unclear financial data,…

Open banking allows SMEs to securely share their financial data with third-party providers capable of assessing credit history. This creates better opportunities for SMEs—especially startups or those with limited credit history—to access financing from a variety of financial institutions.

Enhanced financial management

Through open banking, SMEs can access a wide range of financial products and services from different providers on a single platform. Business owners can view all accounts, transactions, and financial data in one dashboard or app, empowering them to make smarter financial decisions and manage cash flow more effectively.

More competitive pricing

Another positive impact of the open banking ecosystem is the increased price competition for financial products and services. By leveraging the financial data of SMEs, credit institutions can offer financial products that are tailored to the specific needs, size, and sector of each business. This means that SMEs can access the most suitable loan packages available to them.

Stronger security and data privacy

To participate in open banking, banks and third-party providers must comply with strict security standards set by international and national regulations. This ensures that SMEs’ financial data is kept safe, private and protected from unauthorized access.

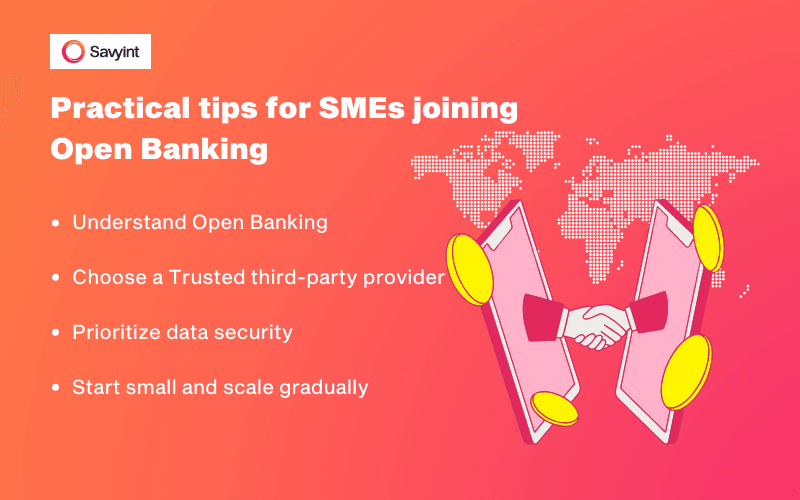

Practical tips for SMEs joining Open Banking

Understand Open Banking

Before joining the open banking ecosystem, it is essential for SMEs to fully understand the nature and how open banking works. Organizations and SMEs can start by reading articles, watching explainer videos, and participating in webinars. It is also valuable to connect with other business owners who have already embraced open banking and learn from their experiences. The more knowledge SMEs gain about open banking, the better equipped they will be to make smart and informed decisions.

Choose a Trusted third-party provider

When entering the open banking ecosystem, SMEs will need to select a third-party provider to manage their financial data. The selection should be based on clear criteria: review the provider’s list of partners, existing clients, and past projects. SMEs can start right away by researching information on company websites, reading customer reviews, and seeking recommendations from businesses that have worked with these providers.

Prioritize data security

Data security should be a top priority when participating in the open banking ecosystem. SMEs must ensure their financial data is protected from unauthorized access or theft by verifying that the chosen third-party provider complies with data protection and information security regulations and standards.

Start small and scale gradually

The technical requirements, infrastructure, and data-sharing demands of open banking can feel overwhelming for SMEs. Therefore, it is advisable to begin with basic services—such as integrating payment solutions—and then gradually expand to more complex offerings like lending and credit services. This approach helps businesses stay in control and gradually adapt before moving to full-scale integration.

Joining open banking marks a significant turning point for SMEs. It not only provides access to better financial products and services but also enables more efficient financial management.

To maximize the benefits of open banking, SMEs need to be well-informed, choose reliable providers, and prioritize data security. By following these best practices, SMEs can fully leverage open banking’s advantages, ensuring stable growth without concerns over funding challenges.

About SAVYINT and the SAVYINT Open Banking Solution

SAVYINT is a global technology company with strong expertise in open banking, data security, and protection across key sectors such as financial services, government, manufacturing, telecommunications, healthcare, education, and media.

With extensive hands-on implementation experience, SAVYINT has launched a comprehensive Open Banking solution that fully meets legal and technological requirements to connect and build an open banking ecosystem. The solution includes:

- SAVYINT Open Banking API – Seamlessly integrates with all systems and provides standardized, ready-to-use APIs.

- SAVYINT Open Banking Portal (Headless) – A central portal that enables third-party providers to register, access, and use open banking services.

- SAVYINT API Management – Supports the design, analysis, operation, and scaling of APIs.

- SAVYINT Consent Management – Collects, manages, and tracks user consent for the collection, use, and sharing of personal data.

- SAVYINT CIAM – Manages and secures customer identities.

- SAVYINT Tokenization – Prevents sensitive data leaks.

- Smart eKYC – Enables remote, paperless identity verification.

Connect with SAVYINT’s experts today to kick-start your open banking strategy!